Entries in aircraft values (28)

MARKETLINE WINTER 2013 EDITION

Vol. 26, No. 4 | Dec. 17, 2013 | Go to Charts

IN THIS ISSUE

Bluebook Perspectives: Pre-owned Market Sends Mixed Signals Throughout Industry

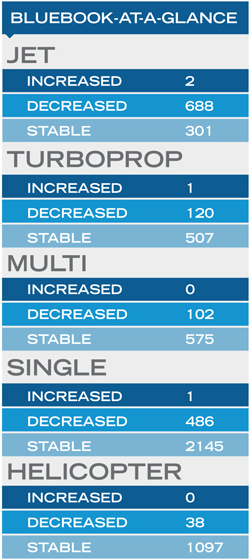

Into the Blue: Aircraft Bluebook At-a-Glance - Cessna Mustang

Ask Aircraft Bluebook: What Does the Trend column in the Aircraft Bluebook represent?

[Download the full Winter 2013 Marketline Newsletter and All Charts.]

Aircraft Bluebook Marketline

Aircraft Bluebook MarketlineCHARTS — Dec. 17, 2013

CURRENT MARKET STRENGTH

;) Click to View Full Size ChartCMS represents an aircraft’s current strength in the market. An A+ rating indicates the aircraft is enjoying a very firm market. Prices for an A+ aircraft are steadily rising, and holding times are very short or nonexistent. At the opposite end of the spectrum, a C- aircraft is one experiencing a very soft market. Its price is commonly discounted, and it often sets on the ramp in excess of eight months before selling. It is important to remember that Current Market Strength is not a forecast. It is valid only at Marketline’s effective date of release.

Click to View Full Size ChartCMS represents an aircraft’s current strength in the market. An A+ rating indicates the aircraft is enjoying a very firm market. Prices for an A+ aircraft are steadily rising, and holding times are very short or nonexistent. At the opposite end of the spectrum, a C- aircraft is one experiencing a very soft market. Its price is commonly discounted, and it often sets on the ramp in excess of eight months before selling. It is important to remember that Current Market Strength is not a forecast. It is valid only at Marketline’s effective date of release.

MARKETLINE FALL 2013 EDITION

Vol. 26, No. 3 | Sept 10, 2013 | Go to Charts

IN THIS ISSUE

Bluebook Perspectives: Value Retention In Today's Market

Into the Blue: Penton Completes Acquisition of Aviation Week Group From McGraw Hill Financial

Ask Aircraft Bluebook: How can I submit information to Aircraft Bluebook?

[Download the full Fall 2013 Marketline Newsletter and All Charts.]

Value Retention In Today's Market:

By Dennis Rousseau | President and Founder | AircraftPost.com

There has been conversation and many questions over the last few years relating to residual values, value retention, value as a percentage of cost new, values coming back, et al. For years, our industry used a 3 to 4 percent annualized depreciation schedule to gauge future values for business jets. Due to the fact our business was in its infancy, we did not possess formidable history to determine the validity of the schedule. When we buy-in to the fundamental assumption that aircraft are depreciating assets with a 30-year life cycle, most business jets will reflect an average midlife (15 years) value retention of 50 percent, when compared to the original cost new.

There has been conversation and many questions over the last few years relating to residual values, value retention, value as a percentage of cost new, values coming back, et al. For years, our industry used a 3 to 4 percent annualized depreciation schedule to gauge future values for business jets. Due to the fact our business was in its infancy, we did not possess formidable history to determine the validity of the schedule. When we buy-in to the fundamental assumption that aircraft are depreciating assets with a 30-year life cycle, most business jets will reflect an average midlife (15 years) value retention of 50 percent, when compared to the original cost new.

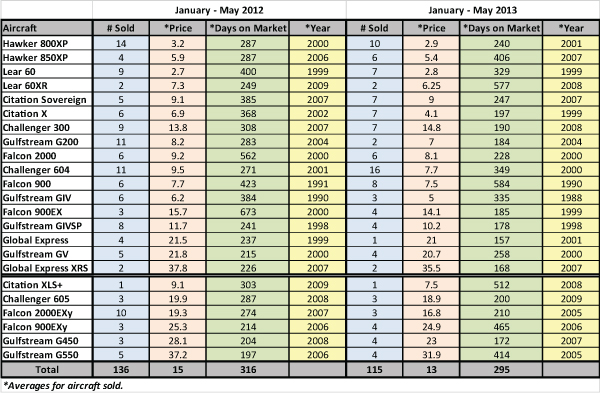

As illustrated in the data sheet, we’ve made every attempt to compare aircraft in an equal light. For out of production aircraft we use a 1999-year model reflecting 14-years in service. For current production business jets, a 2007-year model is used reflecting 6-years in service. Regardless of the term, each make/model is generating nine to ten percent annualized depreciation. For each year through 2013 we’ve calculated the average [pre-owned] selling price for the respective model. The original price new reflects the average contract price for each make/model for the stated year.

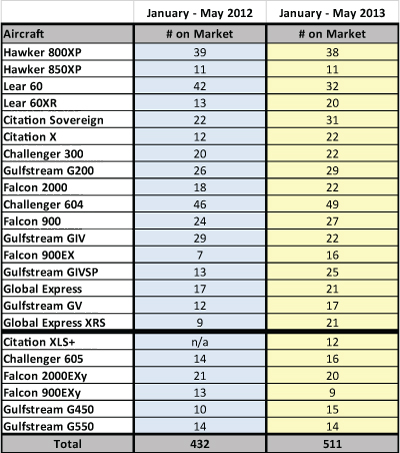

Clearly, these numbers should not be construed as ‘one size fits all.’ Each transaction and make/model comes with its own set of dynamics. However, aircraft with greater capability (higher passenger loads, transcontinental range, increased performance, later generation avionics, etc.) tend to retain a higher percentage of their original cost new. In the majority of cases, there seems to be a corollary between the total aircraft manufactured and lower resale value—the greater the number built, competitive landscape increases and value retention erodes quicker. As of July 2013, AircraftPost calculated an average ten percent of current generation business jet fleets on the market. The range is from 2 percent of the fleet for the G550 to 22 percent for the Lear 60XR. In the case of the former, an anomaly exists. There are now over 425 G550s in-service which would lend one to believe, based on the above-mentioned criteria, that early year models should be retaining less of their original cost new. Current data however, reflects the opposite.

As evidenced recently in pre-owned markets, selling prices continue a downward trend. As newer generation avionics are installed in the next iteration aircraft (i.e., Global Express/XRS/Global 6000; Lear 60/60XR; GIV/IVSP/450, etc.), these newer aircraft will place more pressure on pre-owned aircraft. The rate selling prices decline is determined in part by the above-mentioned and also driven by global economic factors. With the eroding geopolitical situation in the Middle East, South America and Asia, countries like the U.S. and Japan accruing debt of $16 and $10 trillion, respectively, it’s a wonder our markets are generating the sales they are.

Where do we go from here? In a nutshell, if our dollar continues to lose value, the price of most everything goes up. Does that include pre-owned aircraft that have been selling well under ‘normalized markets?’;)

Aircraft Bluebook – Price Digest here for you

Please contact Aircraft Bluebook if you have any specific concern in a particular aircraft market. We will be happy to share with you the most up-to-date information available for your market segment. Call us toll-free at 877-531-1450 or direct at 913-967-1956.

[Go to Charts]

CHARTS — Sept 10, 2013

CURRENT MARKET STRENGTH

;) Click to View Full Size ChartCMS represents an aircraft’s current strength in the market. An A+ rating indicates the aircraft is enjoying a very firm market. Prices for an A+ aircraft are steadily rising, and holding times are very short or nonexistent. At the opposite end of the spectrum, a C- aircraft is one experiencing a very soft market. Its price is commonly discounted, and it often sets on the ramp in excess of eight months before selling. It is important to remember that Current Market Strength is not a forecast. It is valid only at Marketline’s effective date of release.

Click to View Full Size ChartCMS represents an aircraft’s current strength in the market. An A+ rating indicates the aircraft is enjoying a very firm market. Prices for an A+ aircraft are steadily rising, and holding times are very short or nonexistent. At the opposite end of the spectrum, a C- aircraft is one experiencing a very soft market. Its price is commonly discounted, and it often sets on the ramp in excess of eight months before selling. It is important to remember that Current Market Strength is not a forecast. It is valid only at Marketline’s effective date of release.

MARKETLINE CHARTS

;) Click to View Full Size ChartAll of the listed aircraft have a composite score that is presented in the Used Aircraft Market graph. Data points are represented in relationship to the respective new delivered historical price that is equal to 100%. The measure of change is reported in the actual percentage of value in relation to new. The delta between reporting periods can be concluded as the percentage of change.

Click to View Full Size ChartAll of the listed aircraft have a composite score that is presented in the Used Aircraft Market graph. Data points are represented in relationship to the respective new delivered historical price that is equal to 100%. The measure of change is reported in the actual percentage of value in relation to new. The delta between reporting periods can be concluded as the percentage of change.

Click here to download a PDF of the full Marketline Newsletter, including articles and all Charts.

;) Click to View Full Size Chart

Click to View Full Size Chart ;) Click to View Full Size Chart

Click to View Full Size Chart;) Click to View Full Size Chart

Click to View Full Size Chart ;) Click to View Full Size Chart

Click to View Full Size Chart ;) Click to View Full Size Chart

Click to View Full Size Chart ;) Click to View Full Size Chart

Click to View Full Size Chart

MARKETLINE SUMMER 2013 EDITION

Vol. 26, No. 2 | June 10, 2013 | Go to Charts

IN THIS ISSUE

Bluebook Perspectives: YTD Pre-owned Transactions & Prices Continue Down

Into the Blue: Aircraft Bluebook At-a-Glance, Cessna 177 Cardinal Series

Ask Aircraft Bluebook: Where can I find the Aircraft Spec Charts and other infomation formerly in print?

[Download the full Summer 2013 Marketline Newsletter and All Charts.]

YTD PRE-OWNED TRANSACTIONS & PRICES CONTINUE DOWN:

By Dennis Rousseau | President and Founder | AircraftPost.com

When viewing a random selection of pre-owned transactions for the first 5-months of 2013, the number of sales are trending down 15 percent when compared to the same period in 2012. Actual selling prices also are down on average 15 percent, while inventory levels for the same group of business jets has increased 20 percent.

When viewing a random selection of pre-owned transactions for the first 5-months of 2013, the number of sales are trending down 15 percent when compared to the same period in 2012. Actual selling prices also are down on average 15 percent, while inventory levels for the same group of business jets has increased 20 percent.

As you consider these facts we must also take into account other mitigating factors, such as the year of manufacture of the aircraft sold, cost of the aircraft when it was new, the cost new today, as well as nominal depreciation, et al. By way of example, an aircraft that sold new in 2005 for $44 million and today sells for $32 million is not too far off of a 4 percent per year depreciation schedule. From another perspective, it has retained 73 percent of its original cost , which falls in line with a 30-year useful life.

A number of factors continue to affect growth and stability in our industry – some are geopolitical, others are related to the global financial debacle that started in 2008.

Within our industry, where 250 aircraft were once considered a standard production run, we now have 400+ that will eventually compete in the pre-owned market. Therein in the case of ‘over-production’, we face dynamics that were once not a factor, such as eroding residual values. As the business jet fleet ages and pre-owned inventory increases, will pricing continue to erode? What effect will new aircraft pricing and shorter delivery times have on the pre-owned market?

Aircraft Bluebook – Price Digest here for you

Please contact Aircraft Bluebook if you have any specific concern in a particular aircraft market. We will be happy to share with you the most up-to-date information available for your market segment. Call us toll-free at 877-531-1450 or direct at 913-967-1956.