Entries in Dassault Falcon (20)

MARKETLINE WINTER 2012 EDITION

Vol. 25, No. 4 | December 7, 2012 | Go to Charts

IN THIS ISSUE

Bluebook Perspectives: Facing the Nation

Into the Blue: Aircraft Bluebook At-a-Glance, Cessna 152 Series

Ask Aircraft Bluebook: In the aircraft base average lines in the Bluebook we always see the “No Damage History” as a standard requirement, but if there is damage how does the Bluebook reflect this in terms of value?

[Download the full Winter 2012 Marketline Newsletter and All Charts.]

BLUEBOOK PERSPECTIVES:

Facing the Nation

by Carl Janssens, ASA | Aircraft Bluebook — Price Digest

It is all said and done. A new leader has been chosen. The challenges of this executive office are staggering. Creating jobs for the people in his charge, modification of the healthcare system and ongoing issues with a slowing economy are enormous.

It is all said and done. A new leader has been chosen. The challenges of this executive office are staggering. Creating jobs for the people in his charge, modification of the healthcare system and ongoing issues with a slowing economy are enormous.

Yes, the newly appointed leader of the People’s Republic of China, Xi Jinping, faces many complex challenges in the days ahead. Similar to President Barack Obama, how policies will be developed to benefit his countrymen have yet to be revealed. One thing is certain, China is focused on growing its economy, so much so that it is predicted to surpass the U.S. economy in less than five years – or so critics think.

Having visited Savannah, Georgia recently, one would see a boom town of growth. Construction is everywhere around the Gulfstream campus. So, if there are such great opportunities to sell aircraft, why aren’t prices more stable these days? I suggest prices are stable, with the exception of Hawker aircraft, for reasons already clear to the aviation community. OEMs are selling new aircraft and making money.

Dealing with the pre-owned market is a bit more challenging. The pre-owned market is being re-defined by the velocity of transactions. It takes more than just a few transactions to make the pre-owned market move in the right direction. Price is always a concern. Sellers want maximum return on their assets. Buyers want compensation for future values up front — in the form of discounts. Similar to the way politics are supposed to work, somewhere in the middle, at least in the playing field of a deal, a resolution is made and a sale is complete. Both buyer and seller may not be happy, but the best outcome was agreed upon by both parties, while the old adage of economics; supply and demand referee. When it comes to the bottom line, the question should be: was the business tool, the corporate aircraft, a needed asset in growing profits by its ability to move folks in an efficient and timely manner? The answer will always be “yes.” Walking around sock-footed and beltless takes time- and time is money. Sure, things could be better, corporations could become more confident in the economy and make some capital investments in their transportation budget, and a legislative agenda for growing the economy could be revealed by President Obama. But none of that looks like it’s going to happen any time soon. One can always hope for better times, but don’t neglect the opportunities that are still available now.

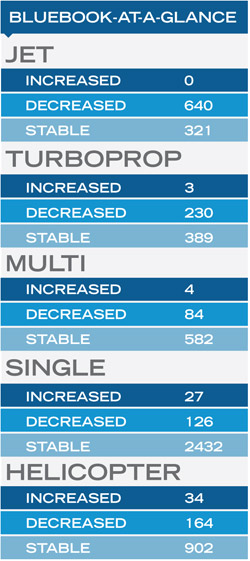

Looking at the BLUEBOOK-AT-A-GLANCE column (page 1) shows a market in motion. Prices for pre-owned aircraft continue to decrease quarter-to-quarter in the jet and turboprop category. Days on market for properly priced aircraft are moving on to new owners in a matter of months. Movement is good.

Fixed wing single and multi engine values remain stable, while the helicopter segment also is reporting a majority of models with no change in values, when compared to the previous quarter. To see what changes have occurred in values, refer to the newly released edition of Aircraft Bluebook – Price Digest®.

Aircraft Bluebook – Price Digest here for you

Please contact Aircraft Bluebook if you have any specific concern in a particular aircraft market. We will be happy to share with you the most up-to-date information available for your market segment. Call us toll-free at 877-531-1450 or direct at 913-967-1956.

[Go to Charts.]

Aircraft Bluebook Marketline

Aircraft Bluebook MarketlineCHARTS — DECEMBER 6, 2012

CURRENT MARKET STRENGTH

;) Click to View Full Size ChartCMS represents an aircraft’s current strength in the market. An A+ rating indicates the aircraft is enjoying a very firm market. Prices for an A+ aircraft are steadily rising, and holding times are very short or nonexistent. At the opposite end of the spectrum, a C- aircraft is one experiencing a very soft market. Its price is commonly discounted, and it often sets on the ramp in excess of eight months before selling. It is important to remember that Current Market Strength is not a forecast. It is valid only at Marketline’s effective date of release.

Click to View Full Size ChartCMS represents an aircraft’s current strength in the market. An A+ rating indicates the aircraft is enjoying a very firm market. Prices for an A+ aircraft are steadily rising, and holding times are very short or nonexistent. At the opposite end of the spectrum, a C- aircraft is one experiencing a very soft market. Its price is commonly discounted, and it often sets on the ramp in excess of eight months before selling. It is important to remember that Current Market Strength is not a forecast. It is valid only at Marketline’s effective date of release.

MARKETLINE CHARTS

;) Click to View Full Size ChartAll of the listed aircraft have a composite score that is presented in the Used Aircraft Market graph. Data points are represented in relationship to the respective new delivered historical price that is equal to 100%. The measure of change is reported in the actual percentage of value in relation to new. The delta between reporting periods can be concluded as the percentage of change.

Click to View Full Size ChartAll of the listed aircraft have a composite score that is presented in the Used Aircraft Market graph. Data points are represented in relationship to the respective new delivered historical price that is equal to 100%. The measure of change is reported in the actual percentage of value in relation to new. The delta between reporting periods can be concluded as the percentage of change.

Click here to download a PDF of the full Marketline Newsletter, including articles and all Charts.

;) Click to View Full Size Chart

Click to View Full Size Chart ;) Click to View Full Size Chart

Click to View Full Size Chart;) Click to View Full Size Chart

Click to View Full Size Chart ;) Click to View Full Size Chart

Click to View Full Size Chart ;) Click to View Full Size Chart

Click to View Full Size Chart ;) Click to View Full Size Chart

Click to View Full Size Chart

MARKETLINE FALL 2012 EDITION

Vol. 25, No. 3 | September 5, 2012 | Go to Charts

IN THIS ISSUE

Bluebook Perspectives: Heat-Thunder and Politics

Into the Blue: Cessna Citations - How to Keep Them All Straight

Ask Aircraft Bluebook: I have a Cessna 340A that has had a RAM VII overhaul & improvement. How do I adjust for this using the Bluebook?

[Download the full Fall 2012 Marketline Newsletter and All Charts.]

BLUEBOOK PERSPECTIVES:

Heat - Thunder and Politics

by Carl Janssens, ASA | Aircraft Bluebook — Price Digest

From a weather perspective, the first quarter of 2012 in Kansas City, wasn’t so bad. What should have been snow and ice, turned out to be an early Spring. Second quarter April showers brought some May flowers, but after that it got hot, really hot – Arizona hot. Or, in the words of Airman Adrian Cronauer in the film Good Morning Vietnam, “It’s hot!” With the heat came … nothing. Mother Nature dried her tear ducts. A severe drought not only ensued, but is still in progress. Not to say there haven’t been occasional claps of thunder, but nothing apart from hit and miss precipitation. The only thing in abundance is politics. As everyone knows by tuning into their favorite media outlet, it is the Olympics of American politics.

From a weather perspective, the first quarter of 2012 in Kansas City, wasn’t so bad. What should have been snow and ice, turned out to be an early Spring. Second quarter April showers brought some May flowers, but after that it got hot, really hot – Arizona hot. Or, in the words of Airman Adrian Cronauer in the film Good Morning Vietnam, “It’s hot!” With the heat came … nothing. Mother Nature dried her tear ducts. A severe drought not only ensued, but is still in progress. Not to say there haven’t been occasional claps of thunder, but nothing apart from hit and miss precipitation. The only thing in abundance is politics. As everyone knows by tuning into their favorite media outlet, it is the Olympics of American politics.

No, this isn’t about weather or politics, but a great metaphor to describe the current general and business aviation re-sale economy.

Talk about heat, the ongoing battle over user’s fees has the interest of general aviation standing at attention. Not that user fees will cause a grinding halt to general aviation, but it will certainly stifle its spirit. That’s not good. Then, there are environmental issues, such as taking the low lead out of avgas in California. Buyers and sellers are keenly aware of these and other issues impacting our aviation marketplace. After these hurdles are cleared, then the aircraft’s time and condition, along with market perception, will make up the sweet spot that makes a deal happen.

Along with the heat, there is a drought. Our industry has been a dustbowl since 2008. Even in a drought, an occasional clap of thunder happens. Not frequently, just here and there. Like thunder, there are similar pockets of activity that continue to bring relief, and more importantly, movement to the pre-owned market. New sales by aircraft manufacturers bring a compounded chain reaction. Market perceptions are related to the amount of activity being experienced in the pre-owned market. Moving the pre-owned inventory entails incredible knowledge and insight on the part of the aircraft dealer/broker. Bluebook help sheets collected from various dealers and brokers, report positive sales activity to others hoping activity will pick up. Just like a summer thunderstorm, it’s a hit and miss scenario.

The presidential and national elections are dragging the economy, including the pre-owned aircraft market. Seems like Wall Street is slumbering in an attempt to wait and see what kind of day with arise on November 6, 2012. At least this election is anticipated to be decisive, and not a repeat of the November 2000 election. What’s good or bad will be decided by the people.

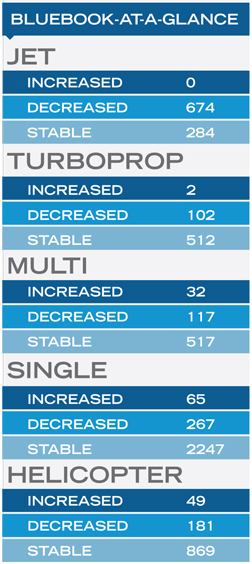

Values have been predictable, as reference in Bluebook-At-A-Glance. A majority of aircraft in the jet category trended downward when compared to summer 2012 Bluebook values. Reasons include: better than average inventories, a buyer’s market, and finance. Turboprops were mostly stable with little trending when compared to the previous reporting quarter. Likewise, Aircraft Bluebook – Price Digest is reporting a stable market for the multi, single and helicopter categories with minimal trending.

Aircraft Bluebook – Price Digest here for you

Please contact Aircraft Bluebook if you have any specific concern in a particular aircraft market. We will be happy to share with you the most up-to-date information available for your market segment. Call us toll-free at 877-531-1450 or direct at 913-967-1956.

[Go to Charts.]

CHARTS — SEPTEMBER 5, 2012

CURRENT MARKET STRENGTH

;) Click to View Full Size ChartCMS represents an aircraft’s current strength in the market. An A+ rating indicates the aircraft is enjoying a very firm market. Prices for an A+ aircraft are steadily rising, and holding times are very short or nonexistent. At the opposite end of the spectrum, a C- aircraft is one experiencing a very soft market. Its price is commonly discounted, and it often sets on the ramp in excess of eight months before selling. It is important to remember that Current Market Strength is not a forecast. It is valid only at Marketline’s effective date of release.

Click to View Full Size ChartCMS represents an aircraft’s current strength in the market. An A+ rating indicates the aircraft is enjoying a very firm market. Prices for an A+ aircraft are steadily rising, and holding times are very short or nonexistent. At the opposite end of the spectrum, a C- aircraft is one experiencing a very soft market. Its price is commonly discounted, and it often sets on the ramp in excess of eight months before selling. It is important to remember that Current Market Strength is not a forecast. It is valid only at Marketline’s effective date of release.

MARKETLINE CHARTS

;) Click to View Full Size ChartAll of the listed aircraft have a composite score that is presented in the Used Aircraft Market graph. Data points are represented in relationship to the respective new delivered historical price that is equal to 100%. The measure of change is reported in the actual percentage of value in relation to new. The delta between reporting periods can be concluded as the percentage of change.

Click to View Full Size ChartAll of the listed aircraft have a composite score that is presented in the Used Aircraft Market graph. Data points are represented in relationship to the respective new delivered historical price that is equal to 100%. The measure of change is reported in the actual percentage of value in relation to new. The delta between reporting periods can be concluded as the percentage of change.

Click here to download a PDF of the full Marketline Newsletter, including articles and all Charts.

;) Click to View Full Size Chart

Click to View Full Size Chart ;) Click to View Full Size Chart

Click to View Full Size Chart;) Click to View Full Size Chart

Click to View Full Size Chart ;) Click to View Full Size Chart

Click to View Full Size Chart ;) Click to View Full Size Chart

Click to View Full Size Chart ;) Click to View Full Size Chart

Click to View Full Size Chart

MARKETLINE SUMMER 2012 EDITION

Vol. 25, No. 2 | June 6, 2012 | Go to Charts

IN THIS ISSUE

Bluebook Perspectives: Thumps and Bumps in the Pre-Owned Market

Into the Blue: 12th Annual EBACE Convention Shines in Geneva

Ask Aircraft Bluebook: Why can’t I find my kit aircraft in the Aircraft Bluebook?

[Download the full June 2012 Marketline Newsletter and All Charts.]

BLUEBOOK PERSPECTIVES:

Thumps & Bumps in the Pre-Owned Market

by Carl Janssens, ASA | Aircraft Bluebook — Price Digest

Optimists see the silver lining behind the cloud while the pessimist only sees the cloud. Optimism continues to be the silver lining in the pre-owned aircraft market. However, reality of the dark cloud dictates an awareness and calculated approach.

Such are the conditions in the current ever-evolving pre-owned market. For the most part, the glory days of aircraft values being treated as premium investment opportunities are now nothing more than a faded memory. Knowledgeable buyers and sellers are keenly aware of this. Change of ownership continues at a slow to steady pace while values for the most part show continued depreciation. The exceptions are late model long range executive business jets.

So, why haven’t values had some sort of rally? The answer still remains in the old school of supply and demand. While inventories for pre-owned aircraft are continuing to deflate ever so slightly, the abundance of low time, well maintained business aircraft available in the open market have an economic impact on what the market will bear on any given aircraft sale price. Throw in more financial regulations on behalf of the lender and the result is a not-so-much-room to rally premium sale prices.

Other economic indicators are pointing to limited domestic growth in the near future. Some predictions include another recession in the coming months, concerns for Homeland Security and the impact it will have on corporate aviation along with the cost of energy (fuel). While all of this is really pessimistic, the reality still remains that this is the environment the pre-owned business aircraft market operates in. It’s our bubble inside the big bubble, so to speak.

The marquis referencing Bluebook-at-a-glance changes on the right is the reality of an average pre-owned market. For machinery and equipment, which aircraft are classified as, depreciation is the norm rather than the exception. For whatever the cause, the effects are recorded as +/- in the average retail column as it relates to the previous (Spring 2012) values of Aircraft Bluebook – Price Digest. In this market, it is important to remember that transactions between buyers and sellers are more important than actual values. Without movement, there is no market.

In the Jet category, there were no aircraft that increased in average retail value in the Bluebook. Most of the decreases were a reflection of weaker sold prices reported. A number of jets did remain unchanged. Most were in the long range late model class of jets.

For the Turboprop category, the 2006 & 2007 King Air C90GT reported modest increases in average retail. For the most part, values remained unchanged. Decreases in reported average retail in this category were merely another reflection of market activity when compared to the previous quarter.

Much was the same for the Multi and Single piston category. Increases in retail value were reported to include legacy models, those manufactured in the 20th century. Stability in pricing when compared to the previous quarter dominated these market segments.

In the Helicopter category, most models remained stable. Component life and condition play a major role in sale prices. Helicopters that reported an increase in average retail included the Eurocopter AS350 series. For the most part, values were unchanged when compared to the previous quarter.

Aircraft Bluebook – Price Digest here for you

Please contact Aircraft Bluebook if you have any specific concern in a particular aircraft market. We will be happy to share with you the most up-to-date information available for your market segment. Call us toll-free at 877-531-1450 or direct at 913-967-1956.

[Go to Charts.]

Such are the conditions in the current ever-evolving pre-owned market. For the most part, the glory days of aircraft values being treated as premium investment opportunities are now nothing more than a faded memory. Knowledgeable buyers and sellers are keenly aware of this. Change of ownership continues at a slow to steady pace while values for the most part show continued depreciation. The exceptions are late model long range executive business jets.

So, why haven’t values had some sort of rally? The answer still remains in the old school of supply and demand. While inventories for pre-owned aircraft are continuing to deflate ever so slightly, the abundance of low time, well maintained business aircraft available in the open market have an economic impact on what the market will bear on any given aircraft sale price. Throw in more financial regulations on behalf of the lender and the result is a not-so-much-room to rally premium sale prices.

Other economic indicators are pointing to limited domestic growth in the near future. Some predictions include another recession in the coming months, concerns for Homeland Security and the impact it will have on corporate aviation along with the cost of energy (fuel). While all of this is really pessimistic, the reality still remains that this is the environment the pre-owned business aircraft market operates in. It’s our bubble inside the big bubble, so to speak.

The marquis referencing Bluebook-at-a-glance changes on the right is the reality of an average pre-owned market. For machinery and equipment, which aircraft are classified as, depreciation is the norm rather than the exception. For whatever the cause, the effects are recorded as +/- in the average retail column as it relates to the previous (Spring 2012) values of Aircraft Bluebook – Price Digest. In this market, it is important to remember that transactions between buyers and sellers are more important than actual values. Without movement, there is no market.

In the Jet category, there were no aircraft that increased in average retail value in the Bluebook. Most of the decreases were a reflection of weaker sold prices reported. A number of jets did remain unchanged. Most were in the long range late model class of jets.

For the Turboprop category, the 2006 & 2007 King Air C90GT reported modest increases in average retail. For the most part, values remained unchanged. Decreases in reported average retail in this category were merely another reflection of market activity when compared to the previous quarter.

Much was the same for the Multi and Single piston category. Increases in retail value were reported to include legacy models, those manufactured in the 20th century. Stability in pricing when compared to the previous quarter dominated these market segments.

In the Helicopter category, most models remained stable. Component life and condition play a major role in sale prices. Helicopters that reported an increase in average retail included the Eurocopter AS350 series. For the most part, values were unchanged when compared to the previous quarter.